Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Local •

June 5, 2026

One-time studio boss, Grammy winner’s $15M Calabasas Estate Tops County’s Luxury Contracts By The Real Deal

A Calabasas estate dubbed Oaktree Ranch topped last week’s luxury homes to go into contract with a nearly $15 million asking price.

As of Tuesday, the sale for the property at 715 Crater Camp Drive was still pending. The 19-acre equestrian estate topped Los Angeles County contracts last week, based on a report compiled by Marcy Roth of Douglas Elliman’s Eklund Gomes team. The Eklund Weekly Luxury Report Los Angeles rounds up single-family homes and condominiums listed in the Multiple Listing Service for $4 million or more and lists the top contracts based on asking price.

The five-bedroom, eight-bathroom home, which spans 7,500 square feet, was listed in November 2024 for $16.5 million — about 9 percent higher than its current ask. Before that, the home was listed and unlisted a couple of times in recent years, and sought nearly $25 million as recently as 2023, according to Zillow.

Westside Estate Agency’s Stephen Shapiro and Kurt Rappaport hold the listing.

If this deal goes through, it will mark the home’s first sale since it was built in 2003 by the sellers, former Warner Bros. co-CEO Robert Daly and his wife, singer-songwriter Carole Bayer Sager. The gated estate includes a gym, offices, swimming pool with a cabana, barbecue area, a lighted tennis court, an eight-horse stable with a stable manager’s office, chicken and pigeon coops, along with goats, ducks and ponies. There’s also a four-bedroom guest house.

Oaktree ranch was one of 14 new signed contracts in L.A. County last week reported by the Eklund Gomes team for a total of $106.3 million in asking volume. That’s down from the same week last year which recorded 20 homes going into contract for a total of $129.3 million.

The second priciest home by listing to go into contract last week was at 712 Walden Drive in

Beverly Hills. Situated in the Beverly Hills Flats, the nearly 5,300-square-foot residence asked about $14 million, or $2,655 per square foot. As of Tuesday, the sale was in escrow for the home which hit the market in late-March. Carolwood Estates’ Marcie Hartley has the listing and declined to disclose the seller.

The five-bedroom, seven-bathroom 1924-built home features a chef’s kitchen, wet bar, garden studio, pool and covered cabana. Since September 2024, the home has been listed for rent three times, each time asking $25,000 per month, according to Zillow. It last sold in 2017 for $8.8 million.

Housing Market •

June 5, 2026

Stay or Sell? How To Make the Right Call as You Age By Keeping Current Matters

At some point, as you start thinking about the years ahead, this question tends to come up:

“Could I stay here long-term… or would it make more sense to move?”

It’s not always urgent. It often shows up in small moments, like going up and down the stairs, keeping up with the maintenance, or just thinking about what the next chapter of your life might look like in this home.

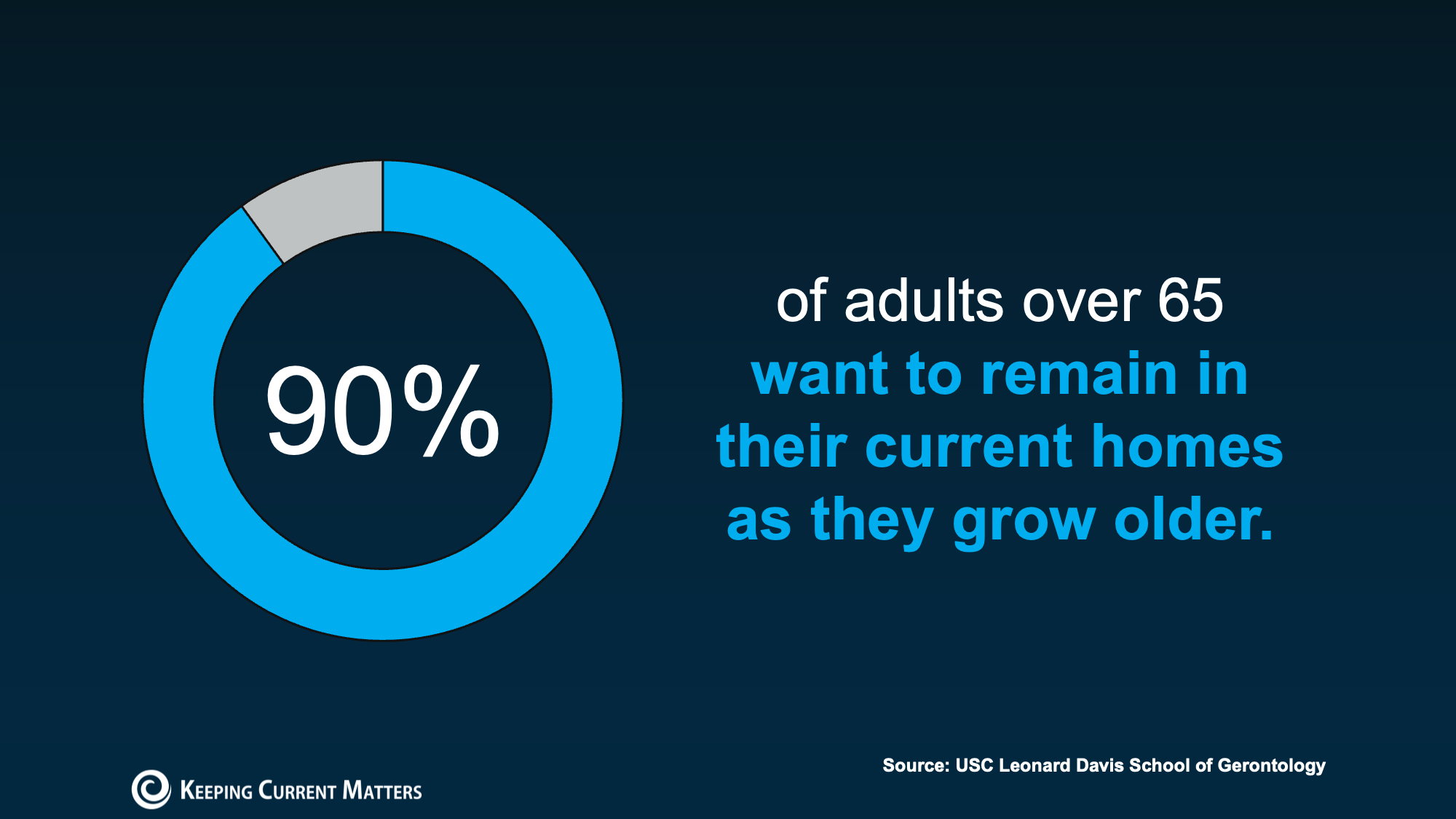

And for most people, the answer is simple. They want to stay.

The USC Leonard Davis School of Gerontology found about 90% of adults over 65 prefer to stay in their homes as they get older (see below):

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

What You Need To Plan for If You’re Staying in Your Home

Aging in place is definitely possible. But it’s better if you have a plan. And here’s why. The home that once worked perfectly may need to change with you over the years. And it’s easier if you can anticipate those expenses.

- Sometimes that means small updates: like adding grab bars in the shower.

- Other times, you’ll have to make bigger decisions: like reworking layouts or moving key spaces to the first floor.

Some of those changes are going to be simple. Others can be a meaningful investment. And that’s why thinking about it early matters. Not because you need to decide anything right now, but because it gives you time.

- Time to understand what your home may need.

- Time to explore your options.

- Time to find the right contractors.

- Time to space out the expense of the upgrades.

According to ElderLife Financial, here’s a rough baseline of what it could cost depending on what needs to be done (see below):

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

Just remember, if you’re thinking about making updates, it’s always worth having a quick conversation before you start. A real estate agent can help you understand which changes tend to make sense for your situation and how they may impact your home’s value based on your local market.

When Moving Might Make More Sense

But staying isn’t always the best fit for every situation. According to Pegasus Senior Living:

“While most seniors hope to age in place, practical considerations sometimes make selling a home the wiser choice.”

Sometimes, it comes down to a simple shift: when the home that once made life easier, starts to make it harder.

That might look like:

- Maintenance or yardwork that’s starting to feel overwhelming

- Stairs or layouts that are getting harder to manage day-to-day

- Or needing more support or care or being too far from loved ones

And sometimes, it’s not about necessity at all. It’s about lifestyle. Some homeowners just don’t want to live through major renovations. Others are ready to simplify, downsize, or move somewhere that better fits this next chapter, whether that’s a smaller home, a 55+ community, or a place closer to family.

For them, moving simply means making daily life easier.

Bottom Line

There’s no one-size-fits-all answer here.

Some people stay and make updates. Others move to simplify things. Either can be the right choice. The goal isn’t to pick one today. It’s to understand your options early, so when the time comes, you feel confident instead of rushed.

And if you ever want a sounding board to think through what the future could look like for you, a local real estate agent is there to help.

Celebrity Homes •

May 30, 2026

Sarah Michelle Gellar and Freddie Prinze Jr. List Their L.A. Home for $10.5 Million By Wendy Bowman

Sarah Michelle Gellar and Freddie Prinze Jr. swapped the tony enclave of Bel Air for a more family friendly footprint in Brentwood‘s Lower Mandeville Canyon pocket in 2013. The A-list couple—who met in 1997 while filming the teen slasher movie I Know What You Did Last Summer and married in 2002—settled with their two young children at a sprawling home set amid rolling lawns on just over a third of an acre. They customized the place through the years, upgrading the swimming pool and converting an attic into a teen hangout complete with arcade machines.

Having already relocated to an Encino property they acquired in an off-market deal in spring 2025 for about $12.4 million, the Buffy the Vampire Slayer star and She’s All That heartthrob are selling the Colonial-style residence they purchased more than a decade ago for $6.1 million. After a short stint on the rental market last year at $60,000 per month, it’s now listed for $10.5 million with Cindy Ambuehl of Christie’s International Real Estate Southern California.

“The home feels safe, private, and part of a wonderful community,” Ambuehl told Realtor.com. “The floor plan is smart and functional, with both a front staircase and a secondary kitchen staircase, which made everyday family living very easy.”

Designed and built in 2006 by Greg and Grace Shain, the husband-and-wife team behind Shain Development, the white board-and-batten-sided and dormer-topped residence offers a total of five bedrooms and six bathrooms. Roughly 7,300 square feet across three levels showcase wide-plank oak floors, custom millwork, and French doors opening seamlessly to the outdoors.

A columned portico entrance leads into a double-height foyer, which flows through large pilastered doorways to a formal dining room dressed in floral wallpaper and a wood-paneled study lined with bookshelves. Further back, a spacious kitchen with a central eat-in island and premium appliances adjoins a casual dining area and a family room, while an elegant fireside living room sports a wet bar and a climatized wine room.

Housing Market •

May 30, 2026

The Real Reason Some People Are Still Moving Right Now By Keeping Current Matters

You may be telling yourself you’re going to wait to move – maybe you’re hoping mortgage rates will come down, prices will fall, or the market will feel a little easier.

And honestly? A lot of people feel that way right now. But here’s what some are starting to realize.

Waiting doesn’t usually fix the thing that made you want to move in the first place.

Your family still desperately needs more room. Your empty nest still feels too…empty.

Your parents or grandparents still need you to live closer.

You just got married… or divorced.

Your vision of retirement has you living somewhere else.

Eventually, life can reach a point where waiting feels harder than moving.

That’s why some people are still deciding to buy right now, even in today’s market. Not because conditions are perfect. But because the life changes behind their move never really went away.

And maybe that’s exactly where you are too. If so, you’re certainly not alone.

The Real Reasons People Move

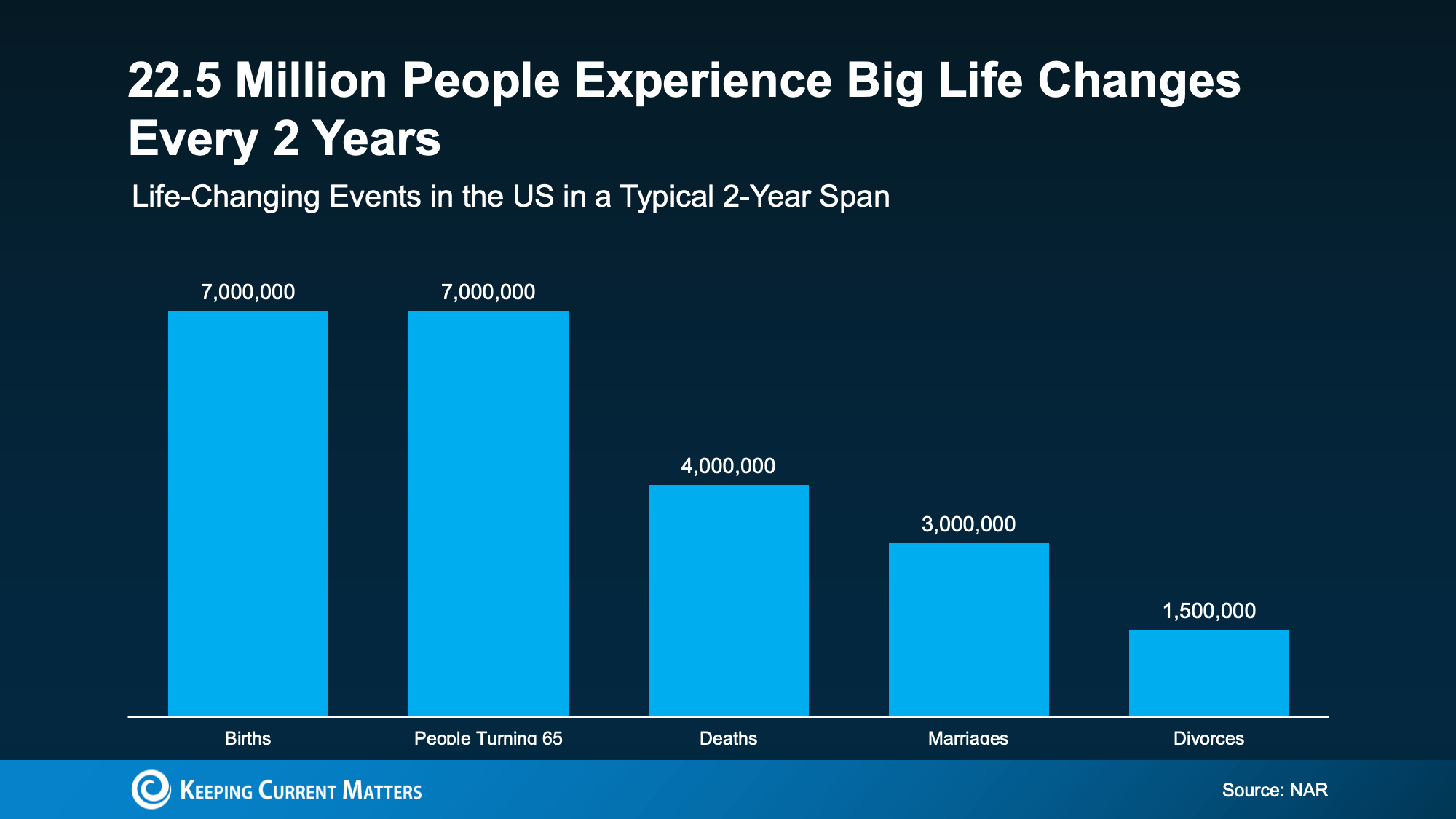

Data from the National Association of Realtors (NAR) shows 1 in 5 buyers last year said they felt like they had to purchase a home at that time, no matter the market.

That’s an important reminder right now. Sure, the dollars and cents of your move have to make sense for you. But big life changes happen whether mortgage rates and home prices are high, low, or somewhere in between.

And those big life events happen more than you may think. NAR says roughly 22.5 million people experience major life changes in a typical two-year span (see graph below):

These are exactly the kinds of things that can change how much space you need, where you want to live, or what kind of lifestyle makes sense now. Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s what makes waiting so hard. Every month you spend hoping the market changes is another month living in a house that no longer works for your life. It’s stressful to feel stuck. And that feeling usually doesn’t disappear.

There May Be More Opportunity Than You Think

But while affordability is still a challenge, there may still be a way for you to make your move.

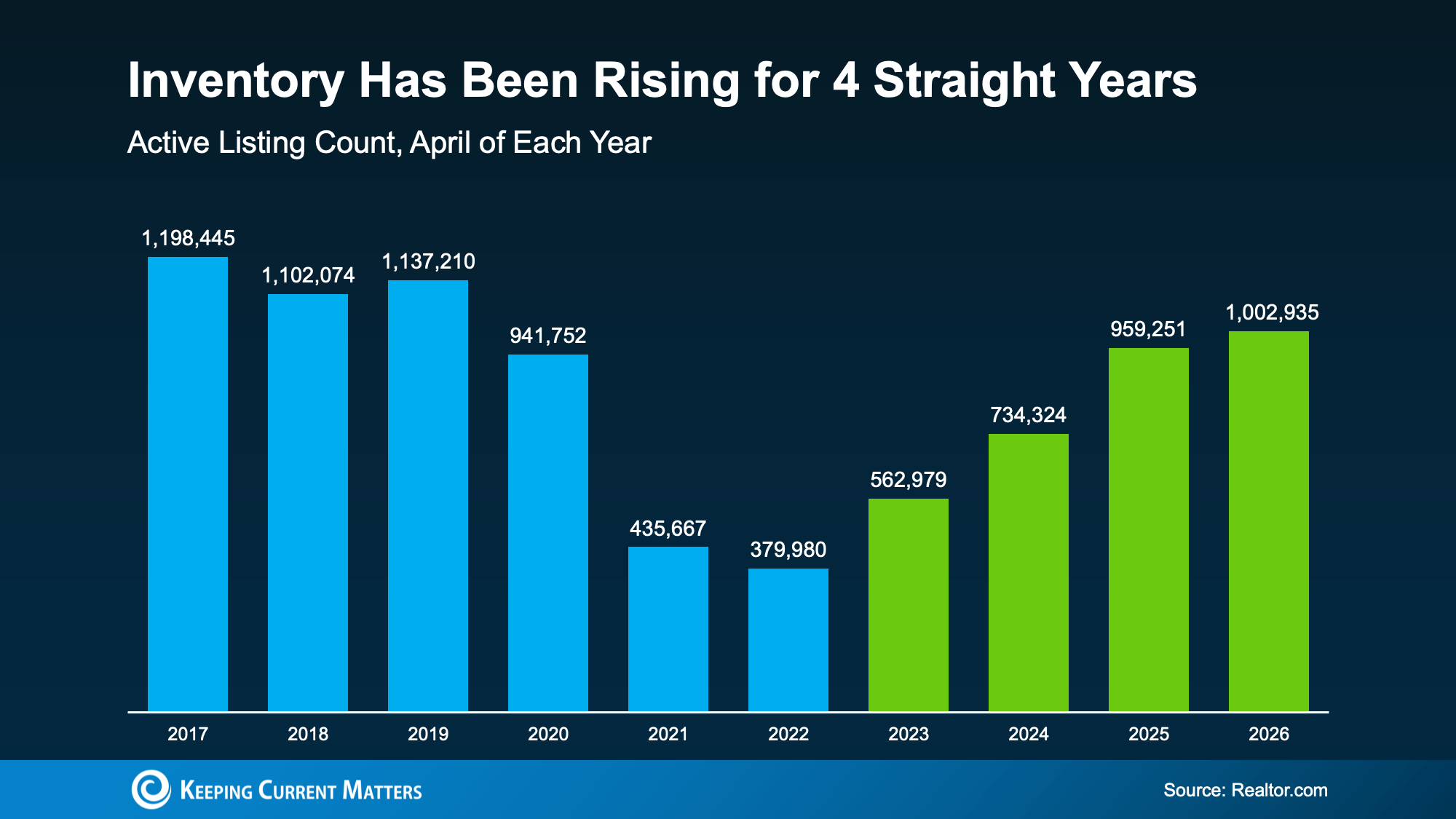

The number of homes for sale has been growing for 4 straight years (see graph below). That means more homes to choose from and, in some markets, more room to negotiate than buyers had just a few years ago.

That doesn’t mean moving is suddenly easy. But it does mean some buyers are finding ways to make a move work. So, if you’ve been putting your plans on hold, maybe the question isn’t just:

“What’s the market doing?” or “When will it get better?”

Maybe ask yourself this, too: “Can I still live where I’m at right now and make it work?”

If the answer to that second question is “no,” it may be worth having a conversation about what your options look like today – despite where rates or prices are. You could find your move is still possible after all. With more homes for sale, there’s a better chance to find one that fits your life (and your budget) right now.

Bottom Line

Life changes. Priorities shift. Families grow. Kids move out. Careers evolve. And eventually, the house you’re in may stop fitting the life you’re living.

If that’s been weighing on you lately, talk to an agent about what your options could realistically look like today, no matter where rates or prices are.

Life can’t always wait for perfect market conditions. Maybe you don’t have to either.

Food •

May 29, 2026

Creamy Shrimp Paprikash By Makenzie Gore

Paprikash, typically featuring chicken, is a Hungarian dish of stewed meat in a paprika-spiced tomato sauce. For an even faster version perfect for weeknights, I decided to add shrimp to this ultra-comforting dinner. It’s one of those meals you can make without really thinking about it—when I have an open can of crushed tomatoes I need to use up, paprikash will always be on the menu. Ready in one pan, this is the dinner that always spices up my weeknights with very little effort required.

I call for Hungarian paprika in the dish because that’s traditional, but you could also experiment with other kinds—try smoked paprika for a slightly different flavor profile, or do a mix of the two. To finish off the sauce, I added sour cream for a bit of tang and extra creaminess. The traditional dish is often served with egg noodles or even dumplings, but for this one, I suggest rice to soak up all of the flavorful, creamy sauce.

Directions

-

- Step 1Pat shrimp dry, then transfer to a medium bowl. Toss shrimp with 1 tsp. paprika, 1 1/2 tsp. salt, and a few grinds of pepper.

- Step 2In a large skillet over medium heat, heat 2 Tbsp. oil. Add shrimp in an even layer and cook, turning halfway through, until cooked through and opaque, 2 to 3 minutes. Transfer to a clean plate.

- Step 3In same skillet over medium-high heat, heat remaining 1 Tbsp. oil. Cook onion, stirring occasionally, until softened, about 7 minutes. Add garlic and cook, stirring, until fragrant, about 1 minute more.

- Step 4Sprinkle remaining 4 tsp. paprika all over skillet and cook, stirring, until fragrant, about 1 minute. Slowly pour in broth while stirring, then add tomatoes. Season with 1 1/2 tsp. salt and a few grinds of pepper. Bring to a simmer and cook, stirring occasionally until slightly thickened, about 5 minutes.

- Step 5Stir in sour cream until combined. Return shrimp to skillet and bring to a simmer. Cook, stirring, until just heated through, about 1 minute; season with salt and pepper, if needed.

6. Step 6 Top with parsley. Serve over rice.

Food •

May 23, 2026

Classic Stuffed Peppers By Rian Handler

How To Make Stuffed Peppers

INGREDIENTS

- Rice: Either works here, though you’ll definitely want to plan ahead if you’re cooking brown rice the same night as your peppers (it can take up to an hour to cook, whereas white usually takes less than 30 minutes). Not a rice cooking pro yet? Follow food editor Taylor Ann’s guides to cooking both brown and white rice, and you’ll be a master in no time.

- Tomato Paste: If you’re like me, every time you need tomato paste for a recipe, you open a can, use a few tablespoons, then pop the can back in the fridge to wait to be thrown away next time you do a fridge clean out. Relatable? You’ve got to try my new hack: whenever you open a can, spoon all the tomato paste from it onto a small sheet pan or plate, then freeze it. Once it’s frozen enough to not stick together, store them in an airtight container. Next time you need just one or two tablespoons, you can use your frozen backstock instead of opening a new can—just cook it for a little longer than you normally would!

- Ground Beef: I usually default to 85/15 (85 percent lean meat and 15 percent fat) or 90/10, but use whatever you like here.

- Diced Tomatoes: I love the convenience of canned tomatoes, but not all are created equal. My favorite brand is San Marzano because I find it to be the most consistent, but other brands will work. Look for ones that have short ingredient lists (just tomatoes, salt, citric acid, and water or tomato juice). I have, on occasion, been known to use fire-roasted or tomatoes with green chiles here, but I never want ones that contain any added sugar or additives.

- Bell Peppers: You can go with any colors here, but keep this in mind: standard red, yellow, and orange are usually a little sweeter than their green or purple counterparts, which lean towards grassier and slightly bitter. Any will work here, but I do recommend trying to buy ones that are similar in size, both height- and width-wise.

- Monterey Jack Cheese: This is my favorite cheese to use here because it’s a little buttery and nutty, but whatever cheese you like works—try cheddar for a sharper, more robust flavor, pepper Jack for a little kick, or even a Mexican blend for a little variety. Though I’m usually a bit proponent of shredding your own cheese, for this family-friendly meal, I’m okay with saying you can use the pre-shredded kind.

- Parsley: This is my preferred garnish, but anything that adds a little pop of green will work here—chives, thyme, even scallions would be great.

STEP-BY-STEP INSTRUCTIONS

Start by preheating your oven to 400°, and making your rice if you haven’t yet. Personally, I like to get my peppers prepped and cut before making the filling, so I don’t have to multitask too much. Here’s how I do it: I cut off the top (using a small paring knife to carve a circle around the stem, kind of like when carving a pumpkin), then I pull out the core and the seeds. I suggest turning the peppers upside down over the sink and tapping them to get the excess seeds out. You could even try rinsing the peppers out if you need some extra help. If a few seeds stay in, don’t panic—it won’t mess up your dish.

Once your peppers are ready, get a large skillet and some oil heating over medium heat. Add your onions, garlic, and tomato paste in stages, letting each one cook a bit before adding the next. You might be tempted to just chuck in your tomato paste with your ground beef, but trust me—letting it cook on its own for a minute or two helps caramelize it and bring out some of its more complex flavors (AND helps get rid of any leftover taste from the can it came in).

Once your aromatics are softened and fragrant, add your ground beef. Cook it, breaking it up with your spoon, until it’s no longer pink (a little under is okay, because it’s going to get baked). Drain the excess oil if needed.

Stir in your cooked rice and diced tomatoes, then add your oregano, salt, and pepper. Taste for seasoning here, then let it cook down for a few minutes until the liquid is reduced a bit.

Home Decor • Housing Market •

May 23, 2026

Why Staging Your House Could Pay Off This Spring By Keeping Current Matters

Selling your house this season? You’ve probably heard you should stage it before it hits the market. But what does that really mean – and is it worth the effort?

The short answer is “yes,” especially right now.

With more houses for sale this year, you’re likely wondering how to make the most money possible without your house sitting on the market. The answer is staging. It can help your house stand out, bring in stronger offers, and sell faster. As Nadia Evangelou, Principal Economist at the National Association of Realtors (NAR), puts it:

“Staging matters. Preparing the home to be ‘buyer-ready’ attracts more buyers, especially now that inventory has increased.”

Here’s what staging actually involves and what it could do for your sale.

What Is Home Staging?

Home staging is the process of preparing your house, so it appeals to as many buyers as possible. That usually means decluttering, deep cleaning, rearranging furniture, and adding simple touches that help each room feel bright, open, and welcoming.

The goal is to help buyers fall in love with the space and picture themselves living there, which makes them more likely to make an offer.

Why Staging Is Worth the Effort

Staged houses tend to perform better on almost every metric that matters when you sell. According to Redfin, staged homes have been shown to sell up to 73% faster than unstaged homes. And they often close in under a month, compared to anywhere from two to three months for vacant ones.

There’s also a strong return on the money you spend.

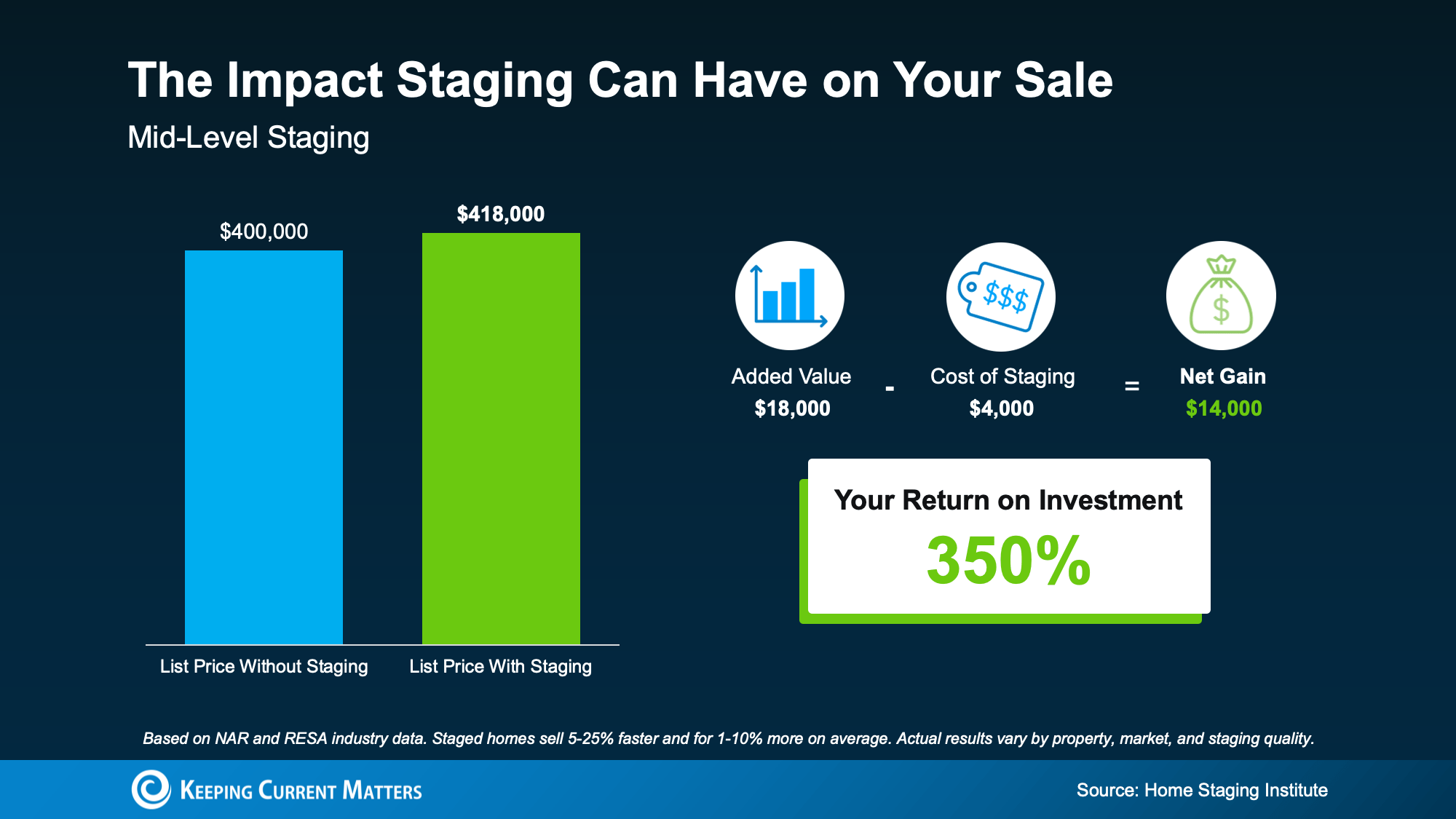

The Home Staging Institute says mid-level staging can deliver a 350% return on investment. On a $400k home, that turns the typical $4k cost into roughly $18k in added value when you sell (see graph below):

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

Your Staging Options

And just in case you’re seeing that $4k upfront investment above and thinking, “I’m not going to spend that,” here’s what you should know.

Staging doesn’t always have to mean hiring a full crew or filling your house with rented furniture. There are a few different paths you can take, depending on your budget and timeline. So, you could spend a lot less and still get a good return.

Here are a few options:

- Professional staging. A stager handles everything from layout to décor, often bringing in their own inventory. According to the Home Staging Institute, costs typically range from $500 to $5k or more, depending on the size of your house.

- Virtual staging. Digital furniture and styling are added to your listing photos, which can be a budget-friendly option for vacant houses.

- DIY staging. If your budget is tight and your home only needs minor updates, decluttering, deep cleaning, and arranging furniture for flow can still make a real difference.

Your agent can help you figure out which approach fits your house, your market, and your goals.

Agents see what buyers respond to in open houses and showings every week, so they can give you specific, personalized recommendations on what’s worth your time and money (and what isn’t).

That way you can get the most bang for your buck – no matter your budget.

Bottom Line

With more homes for sale right now, making a strong first impression matters. Staging can help your house sell faster and for more – and there’s an option for almost every budget.

If you’re getting ready to list, connect with a local real estate agent to talk through what level of staging makes the most sense for your house.

Housing Market •

May 23, 2026

Newly Built Home Prices Hit a 5-Year Low By Keeping Current Matters

If you’ve always assumed a newly built home is just not in your budget, you should know the math just got a little friendlier.

The median sale price of a newly built home is now at its lowest level since 2021, according to the latest data from the Census. And on top of that, builders are still rolling out incentives to bring buyers through the door.

Here’s what’s happening, and what it means if you’re shopping right now.

Prices on Newly Built Homes Have Come Down

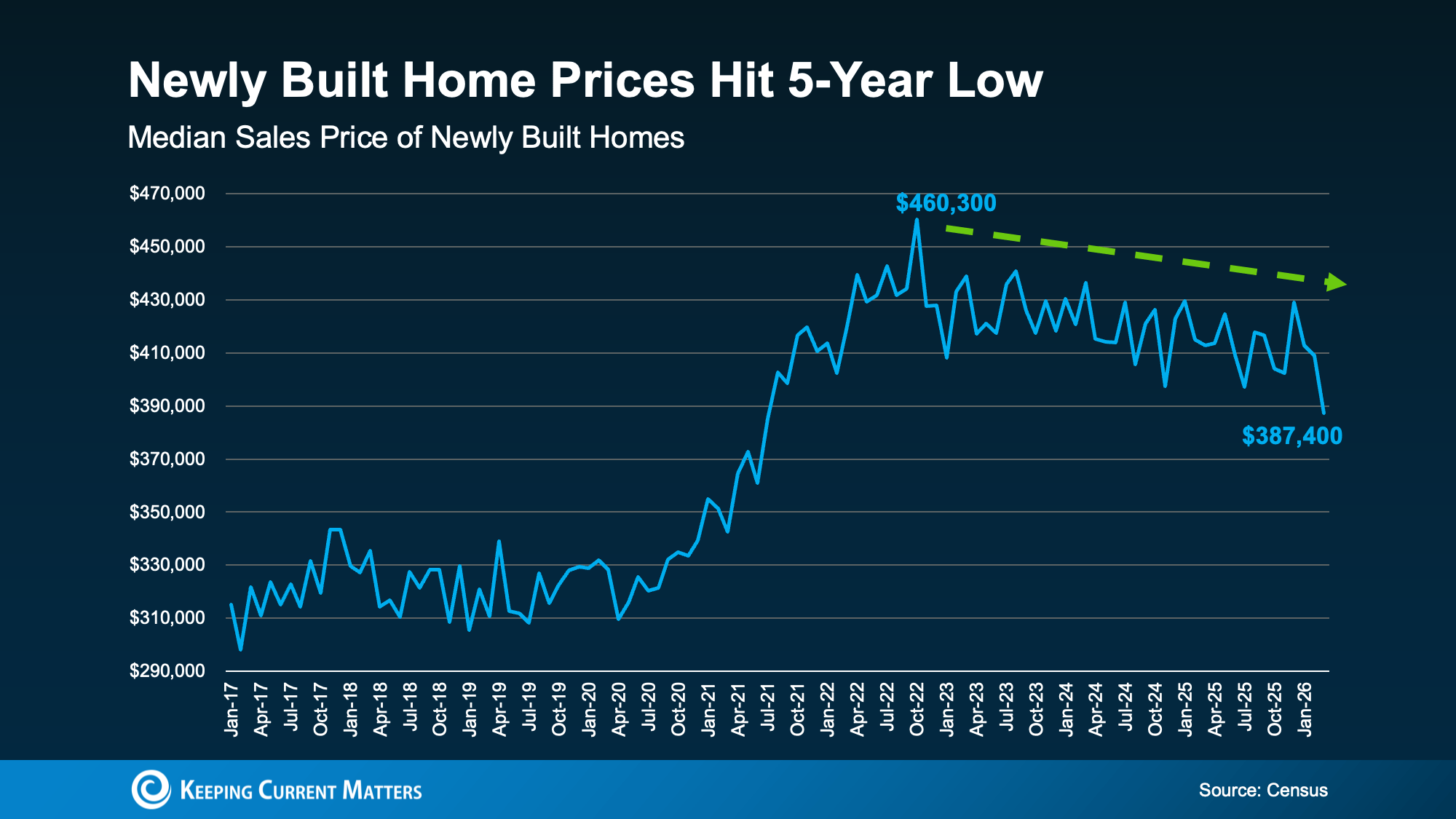

After a steep climb during the pandemic years, prices have eased a bit. The median sale price of newly built homes is sitting at about $390,000. That’s the lowest it’s been in nearly five years (see graph below):

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

That doesn’t mean every home in every market is suddenly affordable. But it does mean that, broadly, you’ll see the best prices on new builds since 2021, if you’re buying now.

Why This Isn’t a Repeat of 2008

And just in case you’re thinking it, lower prices don’t mean the new home market is in trouble. Builders today are being intentional about how much inventory they have, so it doesn’t pile up the way it did in 2008.

If you look back up at the graph, you’ll see that even after the recent improvement in new home prices, they’re still higher than pre-pandemic norms. So, this isn’t a crash. It’s a builder strategy to keep inventory moving.

Homebuilders Are Still Sweetening the Deal

Lower sticker prices aren’t the only break buyers are getting. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers. Those typically include:

- Help with closing costs: Some builders are covering thousands of dollars in fees to reduce the upfront cost of buying.

- Extra upgrades: Think premium finishes, appliance packages, and designer features, often added at no extra cost.

- Mortgage rate buydowns: When the builder pays to lower your mortgage rate, which reduces your monthly payment.

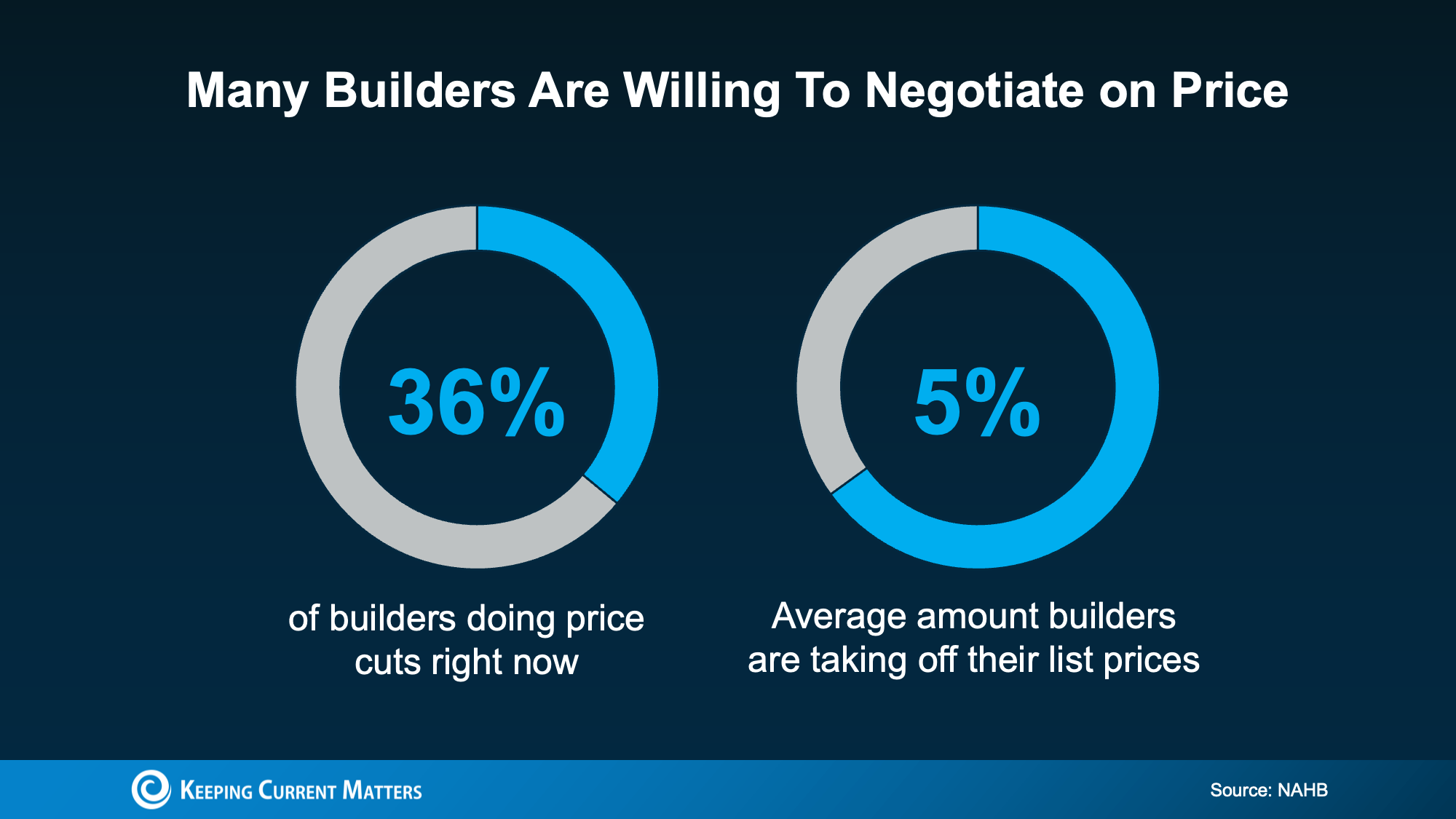

- Price cuts: Over one in three builders (36%) are cutting prices right now, averaging about 5% off list price (see graph below):

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

But builders need to move what they’ve built. That’s a different mindset than a homeowner deciding whether to budge on price. So, you may find they’re more open to adjusting the price than you’d think. As Joel Berner, Senior Economist at Realtor.com, puts it:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

And if you use the version of the graph that shows 2008 prices, you can even reference that in this explainer.

And if here, should I change the last sentence of the lede?

Bottom Line

Builder incentives and lower new home prices are working to your advantage in a way they haven’t in years. Connect with a local real estate agent to see what’s available in your area and what kind of deal a builder may be willing to make.

Local •

May 15, 2026

Inspirational Women of the Valley Honored By Valley News Group

United Chambers of Commerce honored their 2026 Inspirational Women of the Valley today, with a luncheon at The Odyssey restaurant.

The award annually recognizes women of outstanding achievement who have inspired others with their individual stories and accomplishments.

They were chosen not only for their successes, but for how they have inspired others, served as mentors, and through their contributions, made the San Fernando Valley a better place to live.

The five women are Pat Bates, Josie Casarrubias, Jordyn Grohl, Tessa Graham and Chantel Lopez.

Bates is a former CPA and environmentalist who has a long relationship with LAFD. She was named San Fernando Valley Fire Chief of the Year in 2025. She is on the board of the Audubon Society and Chair of the Sepulveda Basin Wildlife Area Steering Committee.

Casarrubias is Director of Rescue Mission Alliance San Fernando Valley, the first woman to hold that position.

Graham is President and CEO of Child Development Institute and advocates at the local and state level for policies that strengthen services for children.

Grohl is a Los Angeles-based community advocate known for her support of charities addressing homelessness and food insecurity in the San Fernando Valley. Alongside her husband, Foo Fighters’ Dave Grohl, she elevates awareness of organizations serving vulnerable populations.

Lopez is Government Affairs Manager for Hope the Mission, and is the liaison between the organization and government entities to address and end homelessness in the valley.

The five honorees were nominated by community members, chambers of commerce and their own organizations. These finalists were chosen by a United Chambers committee composed of previous award winners and community leaders.

United Chambers of Commerce is an association of 14 local chambers in the San Fernando Valley, including Burbank, Calabasas, Filipino American, Granada Hills, North Valley Regional, Northwest Valley, Panorama City, San Fernando City, Sherman Oaks, Encino, Studio City, Toluca Lake, West Valley-Warner Center and Winnetka.

The organization advocates for favorable business policies at all levels of government. For more information visit unitedchambers.org.

Housing Market •

May 15, 2026

4 Ways To Give Your Offer an Edge This Spring By: Keeping Current Matters

Looking to buy a home this season? Here’s what you should know.

Buyers have more leverage today than they’ve had in years. There are more homes to choose from and, in many areas, sellers are more open to negotiation.

But that doesn’t mean competition is gone completely. These days, it varies a lot depending on where you’re hoping to move.

If you’re buying in a popular neighborhood, or in a market where there aren’t many homes for sale, you may still find yourself competing with another buyer.

And that’s especially true in the Spring. Here’s how to stay one step ahead of any competition this season.

Why Your Best Offer Still Matters This Spring

According to experts at Zillow and Realtor.com, Spring is one of the busiest times of year to buy a home.

That’s because many buyers want to move now so they can settle in before the next school year. And when more buyers enter the market, competition naturally picks up.

So, depending on where you’re buying, you may still need to move quickly and make a strong offer, even though the market overall has moderated. And that’s especially true if you find a home you really love.

This is what you need to know to make your offer stand out.

1. Lead with a Strong, Realistic Offer

It’s tempting to start low and negotiate up. And in some markets, that strategy can work. But if a home is priced well and getting attention, lowballing could hurt your chances.

Instead, focus on making an offer that reflects your local market. As Bankrate explains:

“There is no magic formula for an optimal home offer. Any offer will be heavily dependent on asking price and local market conditions . . . Your real estate agent will know the local market well and can advise what a competitive — but fair — offer will look like in your area.”

The goal is to make an offer that makes sense for you and stands out to the seller.

2. Have a Plan for Competing Offers

If you’ve fallen in love with a home, it’s important to have a plan in case there’s competition from another buyer. One strategy your agent may discuss with you is an escalation clause, which Investopedia explains like this:

“An escalation clause is a way to automatically escalate your bid by a certain dollar amount, up to a certain ceiling, to compete with other bids.”

The key is knowing your budget and sticking to it. You don’t want to lose out over a small difference – and this can help prevent that. But you also don’t want to overpay.

Keep in mind that if the appraisal comes in lower than your offer, you may have to make up the difference out of pocket. Your agent can help you weigh those risks and determine the best approach for your situation.

3. Keep Your Offer Clean

Price matters. But sellers also look closely at your offer’s terms. In some cases, a simpler, cleaner offer can stand out – even if it’s not the highest. As Redfin says:

“Sellers tend to want clean, straightforward offers with minimal strings attached. Keep your requests simple and focus on the essentials.”

Your agent can help you prioritize what matters most, so you’re not giving up things you need, while still making your offer as appealing as possible.

4. Be Flexible Where You Can

Sometimes, what helps your offer the most is understanding what matters to the seller. NerdWallet explains:

“As you prepare an offer, you tend to focus on what the seller has (a house) and what you want (their house). But you’ll gain a competitive edge by viewing the transaction from the seller’s eyes: What does the seller want?”

Does the seller need extra time to move out? Or do they want to move as soon as possible? Your agent can talk with the seller’s agent to find out what matters most. Flexibility here can make a big difference in how your offer is received.

Bottom Line

Today’s market may be balancing out, but strong offers still matter – especially during the busy Spring season.

Working with a local agent can help you understand your market and put together an offer that stands out when it matters most.